Linklaters has a series of Quick Guides that provide an overview of key sustainability regimes in the UK, EU and other jurisdictions. Click here to view all our Quick Guides.

This Quick Guide deals with the recommendations and guidance produced by the Taskforce on Nature-related Financial Disclosures (“TNFD”).

Last updated on: 2 June 2026

In a nutshell

The TNFD was created in 2021 and published its final recommendations in 2023.

The TNFD recommendations provide companies and financial institutions of all sizes with a risk management and disclosure framework for identifying, assessing, managing and, where appropriate, disclosing nature-related dependencies, impacts, risks and opportunities.

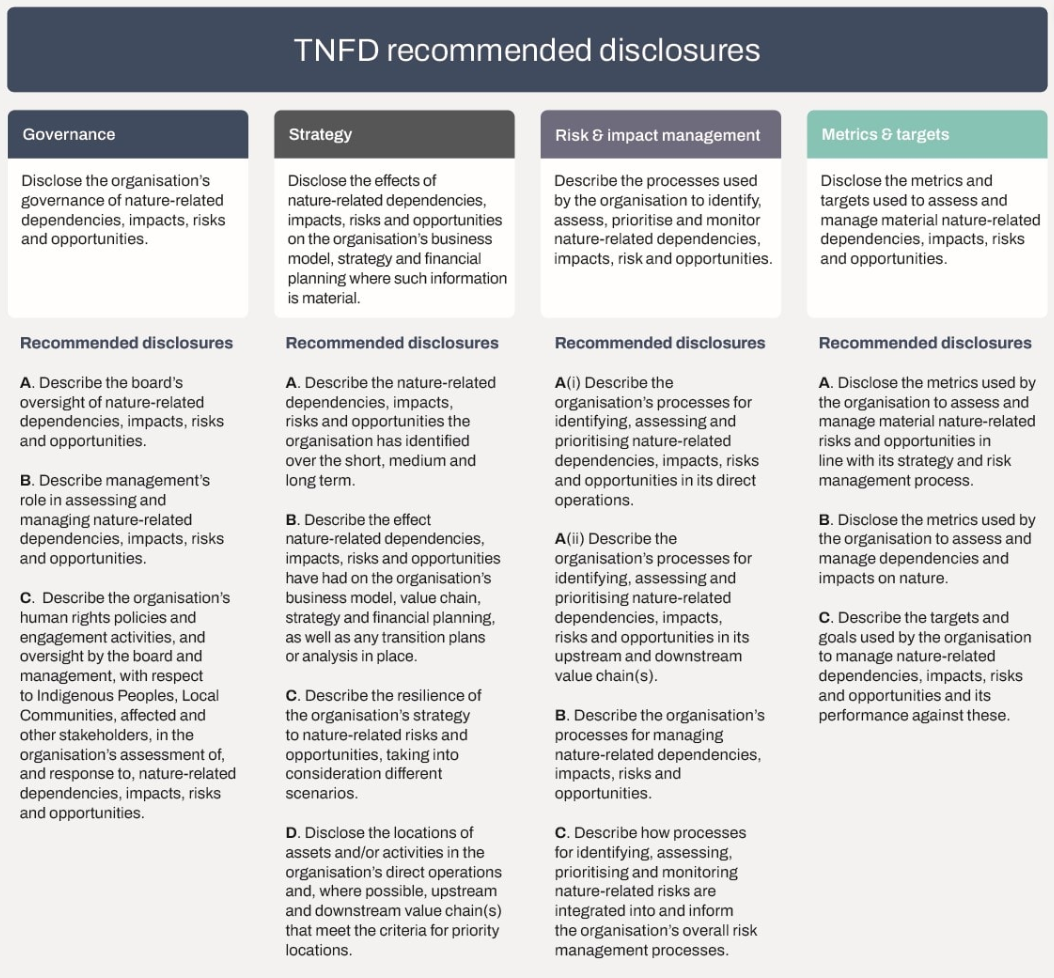

The TNFD framework consists of general requirements and specific recommended disclosures. The recommended disclosures are organised under four pillars: governance; strategy; risk and impact management; and metrics and targets.

These pillars are based on, and consistent with, those used by the well-established climate disclosure framework, the Task Force on Climate-related Financial Disclosures (“TCFD”). Like the TCFD, the TNFD’s recommended disclosures include both qualitative, process-based disclosures, and others that require more quantitative data and analysis.

The TNFD recommendations and guidance have been designed to be used by organisations of all sizes, geographies and sectors.

They are closely aligned with other key frameworks and standards, including the TCFD, the International Sustainability Standards Board (“ISSB”) standards, the Global Reporting Initiative (“GRI”) Standards, and the global policy goals and targets in the Kunming-Montreal Global Biodiversity Framework.

Mandatory or voluntary?

Voluntary

Endorsement in other jurisdictions

The TNFD has not yet been formally endorsed or implemented into national legislation.

However, more than 700 organisations have committed to voluntary reporting of their nature-related issues in line with the TNFD recommendations (see our blog post).

Who does it apply to?

The TNFD is designed for use by corporates, financial institutions, and other organisations across all sizes, geographies, and sectors. This includes SMEs.

However, the TNFD recognises that SMEs may require extra support to apply the TNFD recommendations in a proportionate way. For this reason, the TNFD plans to develop additional guidance specifically to help SMEs.

When does it apply?

The TNFD recommendations were published in final form in September 2023. Any organisation could apply the TNFD framework from that date.

Over 700 organisations across 54 jurisdictions and 62 sectors have registered with the TNFD as “TNFD early adopters”, which means that those organisations are taking steps to make one or more of the TNFD disclosures.

Consistent with the ISSB standards, where an organisation intends to make TNFD-aligned disclosures, these should be published alongside financial statements as part of the same reporting package (subject to any local regulatory requirements otherwise).

What is required?

The TNFD focuses on the disclosure and management of nature-related dependencies, impacts, risks and opportunities, which mean:

- Dependencies – of the organisation on nature;

- Impacts – on nature caused, or contributed to, by the organisation

- Risks – to the organisation stemming from their dependencies and impacts

- Opportunities – for the organisation that benefit nature through positive impacts or mitigation of negative impacts on nature

All 4 types of nature-related issues should be considered by organisations and be covered in the organisation’s TNFD disclosures.

The TNFD framework consists of 6 general requirements, and 14 recommended disclosures. The general requirements are general rules which need to be applied by reporters to create consistency and comparability across reporting.

The general requirements cover the:

- application of materiality;

- scope of disclosures;

- location of nature-related issues;

- integration with other sustainability-related disclosures;

- time horizons considered; and

- engagement of Indigenous Peoples, Local Communities and affected stakeholders in the identification and assessment of the organisation’s nature-related issues.

The recommended disclosures are arranged around 4 pillars (consistent with those used by the TCFD) - see image below taken from the TNFD recommendations:

The TNFD has published guidance to help organisations interpret and apply the TNFD recommended disclosures and the LEAP approach (see below).

Scope

The TNFD recognises that many important nature-related issues will occur upstream and downstream from the organisation’s direct operations. At the same time, the TNFD is aware that reporting on these broader impacts – similar to Scope 3 reporting for climate disclosures – can be complex and challenging for organisations. Therefore, the TNFD permits organisations to choose the scope of their reporting, provided they clearly explain the boundaries they have chosen.

Organisations are also required to clearly identify whether information is relevant to the organisation’s direct operations, upstream value chain(s), or downstream value chain(s).

Time horizons

Organisations are required to define and disclose what they consider to be the relevant short-, medium-, and long-term time horizons.

In doing so, they should take into account the useful life of their assets or infrastructure, as well as the tendency for nature-related risks and opportunities to emerge over medium and long-term periods.

Metrics

The TNFD recommendations require disclosure of:

- A small set of core metrics, consisting of both core global metrics that apply to all sectors, and core sector metrics for each sector – to be disclosed on a comply or explain basis; and

- A larger set of additional metrics, which are recommended for disclosure, where relevant, to best represent an organisation’s material nature-related issues, based on their specific circumstances.

Stakeholder engagement

The organisation should describe its process for engaging Indigenous Peoples, local communities and affected stakeholders about their concerns and priorities with respect to nature-related issues in its direct operations and value chain. The TNFD has developed guidance on meaningful engagement with these groups (see below).

Materiality

The TNFD recommends that organisations use a financial materiality approach (consistent with the ISSB’s definition of material information) to reporting as a baseline.

An impact materiality approach (consistent with the European Sustainability Reporting Standards (“ESRS”) and the GRI standards) can also be used in addition, should the organisation choose or need to do so.

The organisation should clearly state the materiality approach taken and it should apply the same materiality approach for all the nature-related disclosures made.

LEAP approach

To assist organisations in identifying and assessing material nature-related issues, and to facilitate the collection of relevant information for disclosure, the TNFD has developed an integrated assessment tool known as LEAP.

Use of the LEAP approach is not mandatory but is designed to help internal teams develop a robust nature-related approach.

LEAP involves four phases of assessment:

- Locate the interfaces with nature across geographies, sectors and value chains;

- Evaluate dependencies and impacts on nature;

- Assess nature-related risks and opportunities to your organisation; and

- Prepare to respond to nature-related risks and opportunities, including reporting on material nature related issues in line with the TNFD recommended disclosures.

LEAP is designed as an iterative and repeatable process.

Where an organisation already has an equivalent, LEAP can be used as a comparator to ensure that the existing process adequately addresses nature-related risks and opportunities in a way that is aligned with the reporting and disclosure requirements recommended by the TNFD.

Transition plans

TNFD recommended disclosure Strategy B states that an organisation should disclose “any transition plans in place”. Specifically, it states that “organisations that have made nature-related commitments, set nature-related targets, and/or made nature transition plans to address nature-related dependencies, impacts, risks and opportunities to describe their commitments, how they will achieve them and how they are aligned to the Kunming-Montreal Global Biodiversity Framework (GBF) mission, goals and targets”.

In November 2025, the TNFD published guidance on incorporating nature into corporate transition plans, providing a structured framework for managing nature-related risks and opportunities alongside climate objectives. The guidance defines nature transition plans as organisational strategies to halt and reverse biodiversity loss by 2030, aligning with the Global Biodiversity Framework.

The guidance adapts existing climate transition planning best practices, using five key themes: foundations, implementation strategy, engagement strategy, metrics and targets, and governance.

For disclosure, the guidance retains 16 of the Transition Plan Taskforce’s ("TPT") 19 disclosures, replacing climate-specific elements with nature-focused metrics and targets. For more information on the TPT, see our previous blog post.

Companies can either integrate nature into existing climate transition plans or create separate nature-focused plans, though the TNFD recommends an integrated approach where possible.

Scenario analysis

TNFD recommended disclosure Strategy C asks organisations to consider different scenarios when describing the resilience of the organisation’s strategy to nature-related risks and opportunities.

The TNFD has developed guidance on scenario analysis, which builds on the TCFD’s scenario resources, to enable integrated considerations of climate and nature in scenario analysis and integrated disclosures. It also explains how scenarios can be used as part of the LEAP approach (most relevantly in the Assess phase).

The guidance makes clear that quantitative scenario analysis is not required by the TNFD’s recommended disclosures and instead narrative scenarios can be used (for example, the guidance uses scenarios “ahead of the game”, “go fast or go home”, “back of the list”, and “sands in the gears”).

The TNFD is working on developing more advanced nature scenario approaches, including quantitative modelling.

Stakeholder engagement

The TNFD general requirement 6 on engagement states that the “organisation should describe its process for engaging Indigenous Peoples, Local Communities and affected stakeholders about their concerns and priorities with respect to nature-related dependencies, impacts, risks and opportunities in its direct operations and value chain”.

And TNFD recommended disclosure Governance C requires organisations to “Describe the organisation’s human rights policies and engagement activities, and oversight by the board and management, with respect to Indigenous Peoples, Local Communities, affected and other stakeholders, in the organisation’s assessment of, and response to, nature-related dependencies, impacts, risks and opportunities.”

The TNFD guidance states that engagement activities should be done with reference to, and implementation of, the UNGPs, the UN Declaration on the Rights of Indigenous Peoples, and internationally recognised human rights as applicable to affected stakeholders.

Engagement is also an important cross-cutting component of the TNFD’s LEAP approach, informing all phases of LEAP.

ISSB work on nature disclosures

In November 2025, the ISSB announced that it is planning to develop nature-related disclosure requirements, building on its existing IFRS S1 and S2 sustainability disclosure standards (see ISSB press release).

It is not clear at this stage whether this will result in a separate ISSB standard, amendments to the existing ISSB standards or guidance.

The ISSB is aiming to have an exposure draft ready by the next biodiversity conference (COP17) in October 2026 in Armenia.

The ISSB’s work will be subject to public consultation and will draw on the framework developed by the TNFD. The TNFD announced that it will complete technical work in progress by Q3 2026 and pause any further technical guidance in order to support the ISSB (see TNFD press release).

Key documents

- TNFD Recommendations

- How to get started with TNFD, with practical steps, considerations and insights from pilot testing

- The LEAP approach: The identification and assessment of nature related issues

- TNFD sector guidance

- TNFD guidance on biomes

- TNFD guidance on scenario analysis

- TNFD guidance on engagement of Indigenous Peoples, local communities and affected stakeholders

- TNFD guidance on value chains

- TNFD guidance for financial institutions

- TNFD guidance for corporates on science-based targets for nature

- TNFD guidance on nature in transition plans

- TNFD guidance for chief financial officers

- TNFD Glossary

- TNFD Learning Hub

Linklaters materials

- TNFD publishes final recommendations for nature-related risk management and disclosure

- What companies need to know about the final TNFD Recommendations

- GRI and TNFD publish interoperability mapping on nature and biodiversity disclosures

- TNFD and EFRAG publish correspondence mapping

- TNFD announces next wave of early adopters and sector-specific guidance

- New guidance from SBTN on setting science-based targets for nature

- Biodiversity and nature: recent regulatory developments and horizon scanning in the UK, EU and globally

- TNFD two years on: progress on nature-related disclosures

- Next steps on ISSB nature standard and other recent developments

- Linklaters collection of materials on biodiversity and nature

/Passle/5f6c57568cb62a0d7c9eadee/SearchServiceImages/2026-01-28-14-47-21-400-697a2179e8715be98458d80a.jpg)

/Passle/5f6c57568cb62a0d7c9eadee/SearchServiceImages/2026-07-16-14-21-14-425-6a58e8dac8545c9178cdc5a0.jpg)

/Passle/5f6c57568cb62a0d7c9eadee/SearchServiceImages/2026-07-15-14-23-44-624-6a5797f077150555cae1f8fa.jpg)

/Passle/5f6c57568cb62a0d7c9eadee/SearchServiceImages/2026-07-15-08-03-02-583-6a573eb6960adc880fcf7ace.jpg)

/Passle/5f6c57568cb62a0d7c9eadee/SearchServiceImages/2026-07-14-15-58-48-698-6a565cb83b3a0bc7a475319f.jpg)